Title: The psychology of Money

Author: Morgan Housel

Pages: 238

Dear all,

The book was a gift from my brother and it was an interesting read surrounding the topic of investments. There are countless people (finfluencers and professional financial advisers) that will give you advice on which ‘simple’ rules you should follow to build wealth.

Many of these rules are simple and even sound logical when explained why they should be followed, regardless of what situations are happening in the current market. Yet many people will still often act contrary to these rules during certain times (for example when markets are extremely volatile) and afterwards not understand why they acted in a particular way.

This is mostly because we as humans try to make the best decisions with the information that is available to us at each point in time. Our emotions play a significant role in how we conclude to act during unconventional times. For people from the outside, a certain decision will seem flawed, but for the other it will seem more rational. That is why it is important to get an understanding of why and how our emotions can influence our decisions during tumultuous moments and why it is important to retain control of them so we don’t make hasty, irrational and financial costly mistakes.

Here, the following book gives some good insights into the psychology of people when it comes to money and finances.

The book is broken down into the following sections, with some chapters being highlighted for an especially interesting topic:

- Introduction (pg. 1)

- We think about and are taught about money in ways that are too much like physics and science (for which there are rules and laws of nature) and not like psychology (with emotions and behavious) when in fact the latter is what guides us more strongly.

- Physics is guided by laws.

- Money is guided by people’s behaviours

- We think about and are taught about money in ways that are too much like physics and science (for which there are rules and laws of nature) and not like psychology (with emotions and behavious) when in fact the latter is what guides us more strongly.

- Chapter 1 – No One’s Crazy (pg. 9)

- People make decisions at one point in time with the best information available to them. Their intention is to make the decision that will deliver the best possible outcome.

- Yet, another person living at the same point in time, but under other circumstances (and some additional / different information) will possibly disagree with the first person and consider another choice / action / decision to be more appropriate. They will think the first person is silly for making the choice they are.

- People from different generations, raised by different parents, in different parts of the world, born into different economies, experiencing different job markets with different incentives and different degrees of luck, learn very different lessons. For this reason, all of us go through life anchored to a set of views about how money works that varies wildly from person to person.

- Chapter 2 – Luck & Risk (pg. 23)

- Luck and risk are both the reality that every outcome in life is guided by forces other than individual effort. You can’t believe in one without equally respecting the other.

- Yet, both are hard to physically measure accurately.

- The difficulty in identifying what is luck, what is skill and what is risk is one of the biggest problems we face when trying to learn about the best way to manage money. Two lessons should be drawn from this:

- Lesson 1 – Realize that success is not all due to hard work and not all poverty is due to laziness.

- Lesson 2 – Focus less on specific individuals that reached success, but focus more on broad patterns that multiple successful individuals share.

- When things are going extremely well, realize it’s not as good as you think. You are not invincible. If you acknowledge that luck also brought you success then you have to believe in luck’s cousin, risk, which can turn your story around just as quickly.

- Chapter 3 – Never Enough (pg. 35)

- Some people that are worth millions also end up losing their wealth because they made risky financial decisions. The question we should ask is why? Was it because they were desperate for more money?

- A few lessons can be drawn from this:

- Lesson 1 – The hardest financial skill is getting the financial goal post to stop moving. When you earn more money, your desire to have more things moves further to the right. Thus, learning not to move the post further right when you earn more money will make more money available for investments.

- Lesson 2 – Social comparison is what makes us increase our standard of living. In the 60s USA there were the “Jones'” next door to whom we compared our lifestyles with. Today, we are able to compare our lifestyles with everyone around the globe.

- Lesson 3 – Having “enough” does not translate to being conservative. It simply means that by buying and consuming more we will no longer feel happy with each additional purchase, but rather regret.

- Lesson 4 – There are many things that are never worth risking, no matter the potential gain. Your best shot at keeping those things that are invaluable to you (i.e. reputation, freedom, family and friends, being loved, happiness) is knowing when it’s time to stop taking risks that might harm them.

- Chapter 4 – Confounding Compounding (pg. 45)

- You don’t need tremendous force to create tremendous results.

- Good investing isn’t necessarily about earning the highest returns. It’s about earning pretty good returns that can be repeated for the longest period of time.

- Chapter 5 – Getting Wealthy vs. Staying Wealthy (pg. 55)

- Getting money is one thing. Keeping it is another.

- Getting money requires taking risks and putting yourself out there.

- Keeping money requires the opposite of taking risk. It requires frugality and an acceptance that past success can’t be relied on to repeat indefinitely.

- A survival mentality is key with money.

- When making investment decisions, those decisions should not lead you to become financially ruined. The decisions should have been made with “room for error” since unpredictable events can occur during unpredictable events.

- Giving yourself that “room for error” could be what allows you from suffering financial ruin or simply going through a longer financial dip until the market recovers.

- This room for error is the same principle as the well know “margin of safety”.

- It allows you to live happily with a range of different and unpredictable outcomes.

- Investors will do well when they maintain a state of ‘sensible optimism’. This is the belief that the odds are in your favour and that over time things will balance out to a good outcome, even when it happens between moments of misery. Thus, maintaining a good balance between optimism and paranoia is what keeps our expectations and actions realistic.

- Getting money is one thing. Keeping it is another.

- Chapter 6 – Tails, you Win (pg. 69)

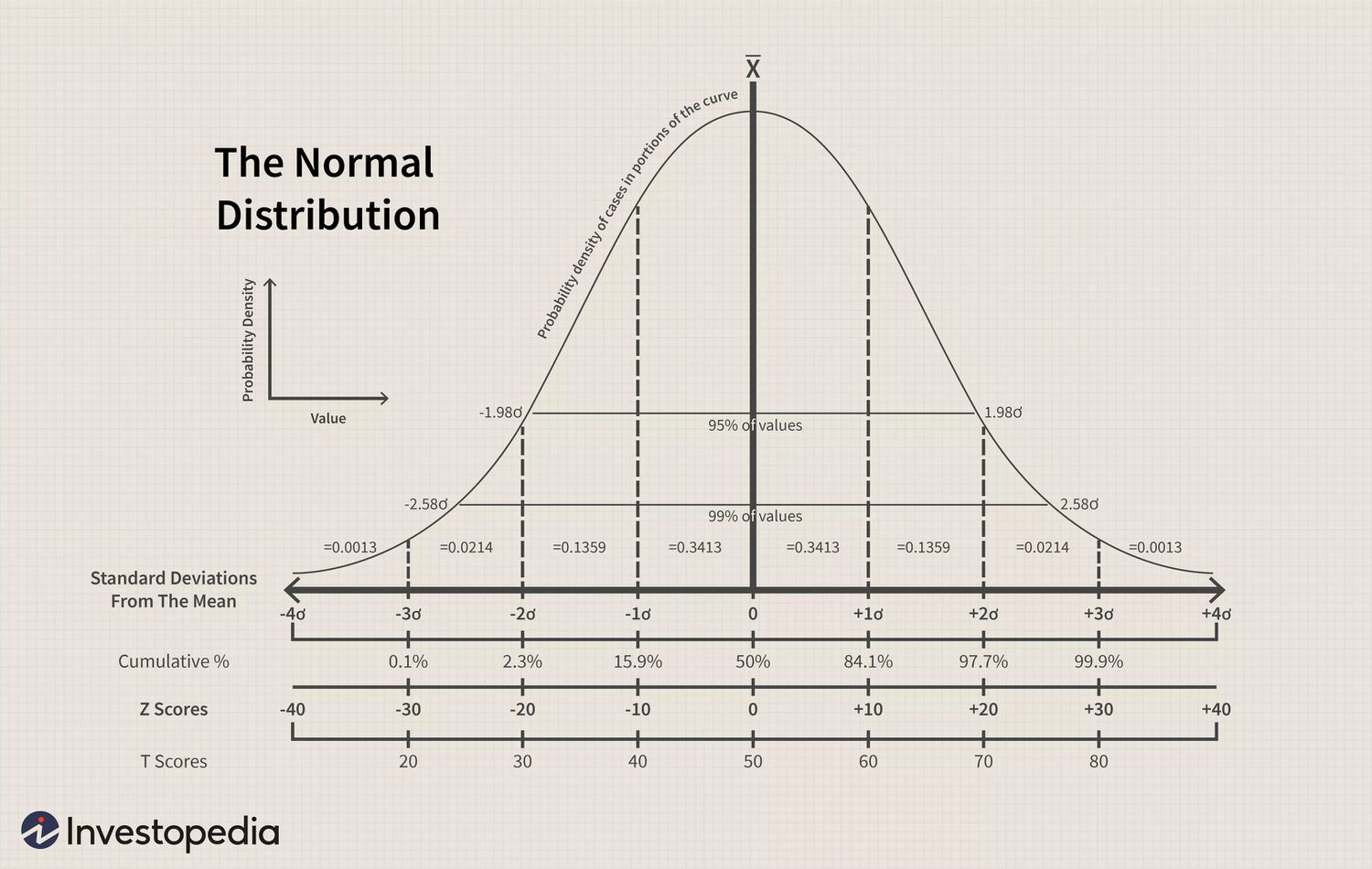

- In business (and investing) a lot of events will happen on a daily and yearly basis that change the world. Yet there will only be a few events that will account for the majority of changes in the world.

- Imaging a bell curve that shows all the events. Majority of events happening will be closer towards the middle and contribute to changes in the world, but only in minor proportions.

- But few events will occur that will be responsible to change a lot of how the world works. These are the tail events.

- Tail Events – with companies

- Finding the company and investment that will bring forth one such change is very difficult. Therefore, by holding a diversified portfolio, you hold a portfolio not only to diversify away from the risk of one investment, but also to potentially catch one of these companies that will bring forth a tail event.

- The lesson from this is that many investments in public companies will bring in a reasonable return, but only few will bring an extraordinary return.

- Tail Events – with investment decisions

- Taking another perspective, the (investment) decisions you make today, tomorrow or next week will not matter nearly as much as the decisions you take on the small number of days when everyone around you is going crazy.

- Your success as an investor will be determined by how you respond to punctuated moments of terror. Thus, not every day is a day to make significant investment decisions, but only on few days when wonderful opportunities make themselves available for a brief moment of time.

- Thus, most days will be OK days to make investments, but plenty will be bad.

- In conclusion, when looking up to some successful investors we often overlook that the most gains from their success came from a small percentage of their choices.

- Chapter 7 – Freedom (pg. 81)

- Aligning money towards a life that lets you do what you want, when you want, with whom you want, where you want, has an incredible return.

- Chapter 8 – Man in the Car paradox (pg. 91)

- When you see someone owning an incredible luxury item (for example a luxury car) you don’t necessarily look at the person and think what he did to get the car. You look at the car and think that you would look great in the car and others will think you are great too.

- The irony of that people tend to want wealth to signal to others that they should be liked and admired. But in reality those other people often bypass admiring you, not because they don’t think wealth is admirable, but because they use your wealth as a benchmark for their own desire to be liked and admired.

- People generally aspire to be respected and admired by others using money to buy fancy things. Yet these things will bring less of it. Instead humility, kindness and empathy will bring you more respect.

- Chapter 9 – Wealth is what you don’t see (pg. 95)

- We tend to judge wealth by what we see, because that’s the information we have in front of us. We rely on outward appearances to gauge financial success.

- Yet, the only way to be wealthy is to not spend the money that you don’t have.

- Rich is a current income.

- Wealth is income not spent. It’s value lies in offering you options, flexibility and growth to one day purchase something that holds more value to you.

- Chapter 10 – Save Money (pg. 101)

- Some money lessons

- Building wealth has little to do with your income and everything to do with your savings rate.

- Learning to be happy with less creates a gap between what you have and what you want.

- You can spend less if you desire less. You desire less if you care less about what others think about you.

- Saving does not require a goal of purchasing something specific in the future. You can save, just for saving’s sake.

- Some money lessons

- Chapter 11 – Reasonable > Rational (pg. 111)

- Do not aim to be coldly rational when making financial decisions. Aim instead to be pretty reasonable. Reasonable is more realistic and you have a better chance of sticking with it for a long run.

- Chapter 12 – Surprise! (pg. 121)

- History helps us calibrate our expectations, study where people tend to go wrong and offers a rough guide of what tends to work. However, it is not, in any way, a map of the future.

- Investors and speculators have feelings and different expectations about companies in the future, for which reason it’s hard to predict what they will do based on what they did in the past.

- Preferences for goods and services change with culture and generations. They will always change.

- There are two dangerous things that happen when you rely too heavily on investment history as a guide to what’s going to happen next:

- 1. You will likely miss the outlier events that move the needle the most

- The most important events in historical data are the big outliers. They are what move the needle. Outlier events play an enormous role because they influence so many unrelated events.

- The majority of what’s happening at any given moment in the global economy can be tied back to a handful of past events that were nearly impossible to predict.

- 2. History can be a misleading guide to the future because it doesn’t account for structural changes

- What we know about investment cycles and startup failure rates is not a deep base of history to learn from, because the way companies are funded today is such a new historical paradigm.

- Tools and techniques that were used to run businesses and used to value businesses are not all completely relevant to today’s world anymore, because different metrics are looked at to value companies.

- Therefore, an interesting quirk of investing history is that the further you look back, the more likely you are to be examining a world that no longer applies today. Since economies evolve, only the most recent history is often the best guide to the future.

- 1. You will likely miss the outlier events that move the needle the most

- Chapter 13 – Room for Error (pg. 135)

- Something important to consider when managing money is to always make room for error.

- The wisdom in having room for error is acknowledging that uncertainty, randomness and chance are an ever-present part of life. Room for error lets you endure a range of potential outcomes and endurance lets you stick around long enough to let the odds of benefitting from a low-probability outcome fall in your favour.

- Therefore, the person with enough room for error has an edge over the person who gets wiped out when they’re wrong.

- You have to take risk to get ahead, but no risk that can wipe you out is ever worth taking.

- You can plan for every risk except the things that are too crazy to cross your mind. Those crazy things can do the most harm, because they happen more often than you think.

- Chapter 14 – You’ll change (pg. 147)

- During your life, you will make constant changes to plans you had made in the past for the next few years. Planning to move for a job but then later moving again are things we cannot plan ahead for. It’s just natural.

- However, in order for the returns of your investment to compound to a wealthy sum, the invested capital plus reinvested returns should be left uninterrupted to bring the most returns possible.

- “…the first rule of compounding is to never interrupt it unnecessarily…” – Charlie Munger

- Chapter 15 – Nothing’s Free (pg. 155)

- Chapter 16 – You & Me (pg. 165)

- There are different players at the stock market. Each player has their own strategy to make returns from their investment. Some play short whilst others play long. Therefore, it is crucial for you to understand which game the other player is playing, so that you don’t fall for their tactics.

- Long term investors invest for returns in the long run whilst short term investors try to profit from short term trades.

- Bubbles form when the momentum of short-term returns attracts enough money from long-term investors.

- Few things matter more with money than understanding your own time horizon and not being persuaded by the actions and behaviours of people playing different games.

- Chapter 17 – The Seduction of Pessimism (pg. 175)

- Chapter 18 – When You’ll believe Anything (pg. 189)

- Chapter 19 – All together Now (pg. 203)

- Chapter 20 – Confessions (pg. 211)

- Postscript – A brief history of Why the US Consumer thinks the way they do (pg. 221)

I definitely took something away from the book and hope that you will as well. The stock market is not necessarily a gambling station if approached and worked appropriately.

Summary:

The book gives good examples and lessons in small and easy to read chapters. The examples are relatable and not complex as you would find in research papers. The lessons given are a good summary of what every investor should take with them before approaching the stock market but also why it is important to invest money in forms other than on their bank account. For this the book will receive a rating of 4.8/5.

Happy holidays! 🙂

Link (German): https://amzn.to/49cLI7E

Link (English): https://amzn.to/4pX1Kd7