Title: Lass die Krise kommen

Author: Ralf Muller

Pages: 226

Dear reader,

I have stumbled upon an interesting book in the library and it did not disappoint. It cites the importance of investing during crises times, not with the goal of short term speculation, but rather buying up what has become cheaper than its ‘true value’.

The book is broken down into the following chapters:

Introduction (pg. 11)

Key items to become a successful investor include: (i) a long time horizon and (ii) compound interest effect.

After a decade or more, the short term volatility cycles become less important to your portfolio.

Crises even prevent people from engaging with the stock market, which is one of the times when investors could enjoy the best time to build wealth. Especially in times of crises more wealth can be made in shorter spans of time than during other calmer phases.

Chapter 1 – Crises are not just negative (pg. 15)

Crises will always come again on the stock market. The objective of the investor is to identify when there is a crisis going on and then to invest anti-cyclical. While mass investors panic and leave the market, you should determine whether there are valid claims for the sell off (for e.g. fraud) or whether it relates to an over-reaction (sales % didn’t grow as much as hoped, but was still positive). If the sell off is an over-reaction, then you should use the crises to your advantage and not let the opportunity pass.

What types of crises could there be?

- High inflation

- Tax increases

- Global supply chain problems

- Economic wars

- Real estate bubbles

- Financial crises

It is especially the bigger crises in the world that present the best opportunity to build wealth, since more people are participating in the ‘frenzy’.

What happens during a crisis?

- The price of a stock and the value of a stock become strongly disconnected from one another

- Price is what the stock is currently selling for

- Value is what the stock is really worth (i.e. if the company were liquidated and all assets (tangible and intangible) were sold off)

How the price determined?

- Supply and Demand, that simple.

- If more stocks are put up for sale, the price of a stock drops.

- If more stocks are sought for purchase, the price of a stocks rises.

- People will decide whether to buy or sell.

What happens after a crisis?

- There are crisis winners and crisis losers.

- The crisis winners are the people that bought stocks for (price) for less than they are worth (value)

- The crisis losers are the people that sold stocks for a loss and whose wealth has dropped.

- Effectively, wealth has only transferred hands.

Which assets are crisis losers and which are crisis winners?

- Paper money is a crisis loser. When things become more expensive it means that the money in the bank has lost purchasing power.

- Paper money does not have an inner value.

- Stocks, precious metals and real estate are some of the crisis profiteers. During a crisis, the price may drop, but generally afterwards, the price returns closer to its inner value.

- These assets cannot be printed into infinity (as is the case with paper money), for which reason they will always have an inner value.

Therefore, paper money should not be saved to build wealth, but should instead be used to acquire assets that will generate wealth.

Chapter 2 – The crises of our time (pg. 36)

The crises of recent (2020s, 2008, 2000) may have an individual say, that theses crises were different, however, they have many things in common. One of them being, that they come to an end.

The world economy is so connected and dependent upon one another that a small ripple in one economy could potentially affect other countries’ economies hard as well.

The small ripple could result from:

- political reasons

- natural catastrophy

- monetary reasons (debt, deficits)

- other

It is exactly these crises that present the ‘buy signals’ that crises investing is about.

People that don’t have a strategy for such events are more unsure what to make of the crises and rather sit passively on the side.

People that have a strategy for such events know that now is the time to be active and invest where asset prices have been pushed down lower than justifiable.

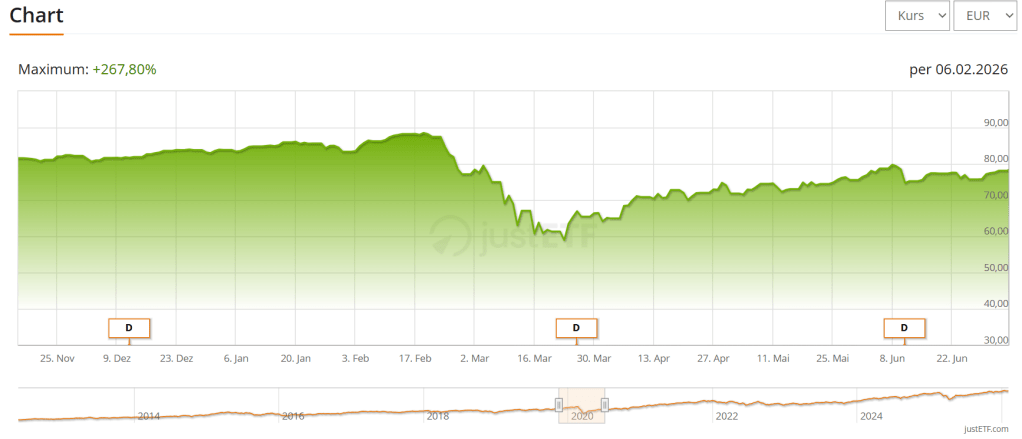

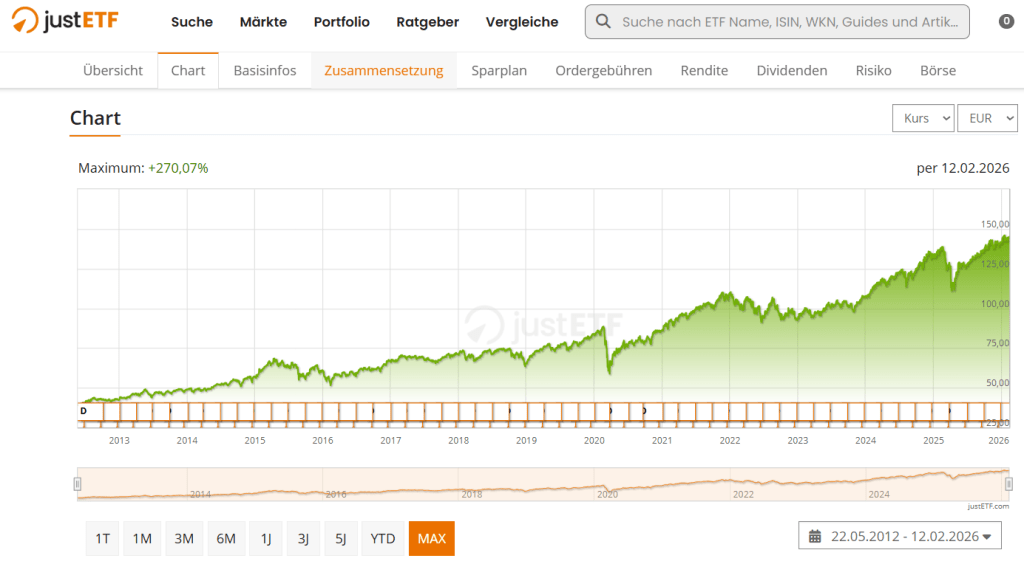

During the time of Corona (2020s) the stock indices around the world, crashed drastically in a short time. However, only weeks after, it started to grow again and has made significant returns since then (see below ISIN IE00B3RBWM25 – Vanguard FTSE All-World UCITS ETF):

2020

Since 2020

Why should you invest?

- Next to the reason of money losing its purchasing power is also the pension gap.

- Many western economies will struggle to pay the pensioners with a suitable and livable pension.

- More worrisome is the outlook for the younger generations that still have their pension days ahead of them in the distant future.

- To counter this problem, and to have more freedom, you should invest money that will work for you whilst you don’t need it so that when you enter retirement, your saved up money is now available to you and the pension money from the state is merely a bonus 🙂

As young individuals we have much potential, life time and energy to build up wealth to become financially independent. The important thing is to start immediately.

There’s a saying: The best time to invest is 10 years ago. The second best time to invest is today.

Chapter 3 – Preparation for crises requires taking responsibility and courage to make decisions (pg. 54)

Time is an immensely important factor. Even more important than a lot of money.

Unfortunately at the young age, consumption is at the centre of many lives. Yet it is very important to become disciplined to invest regularly and uninterruptedly from the moment the first pay cheques start hitting the bank account.

- One clever approach is to “pay yourself first” and don’t invest only what’s left at the end of the month.

If you are not able to work yourself up to a salary of 1 million, then you need to make use of the compounded interest effect. This effect only makes this possible if you give it enough time to work for you.

True, you should be sceptical whether the growth rates on the MSCI World index of between 7% – 9% p/a can be repeated in the future as well. Nothing is guaranteed. However, it is definitely better to give a chance with investing and growing wealth than leaving money in the bank and letting it slowly become devalued through inflation.

What is lifestyle inflation?

- When you start earning more money we inadvertently start using more money for consumption. We might still invest the 10% we set ourselves as a goal, however, we also spend more.

- To go against this we should continue living on the same budget as before, allocate more of the salary rise to investing and some to other expenses. That way, we will reach our investment goals much sooner.

Can our direct environment have an impact on our actions?

- We are who we associate with. If you surround yourself with people that only talk negative of investing, then you would likely not make such a move.

- Therefore, inform yourself expertly (by reading, watching webinars, taking a course, etc.) to learn from this topic outside your current field of friends and associates.

Personal beliefs

- Either your parents, your friends or others have contributed in forming and shaping your beliefs about money. If some of those beliefs are wrong, then it is best to remove them from your vocabulary and replace them with beliefs and truths that are true.

- Negative belief – You don’t talk about money

- Positive belief – With money you can do good things

Investing intuitively vs cognitively

- Sometimes we are confronted with a situation where we need to make a decision, yet we don’t know exactly much about the topic. The logical decision would be to study the topic, consult someone or learn more before making a decision. However, because that takes time, we often revert to relying on our gut (past experience).

- Since you are investing your money for your future, you should counter your reflex of trusting you gut immediately and instead use your cognitive abilities to learn more to make an informed decision.

- Remove emotions from the decisions!!!

- This does not mean you should not trust your gut, but with investing in stocks, investing spontaneously can be costly.

Chapter 4 – The investment strategy to prepare for crises (pg. 77)

The core message: Buy assets for less than they are worth!

Wealthy individuals have made use of the volatility of the stock markets during crises to build significant wealth. Whilst others were selling, they were buying assets with an internal value for a cheaper price. This may be hard (to buy when everyone else is selling), however, this is possible if you have faith and strong belief that the prices will eventually return to a true price / higher than when they dropped down.

- It doesn’t matter, how long after its drop it will take to rise again, the fact that you can buy it cheaper than it’s worth is enough consolation to consider a buy move.

Timing!

- It is not really possible to spot the next “Amazon” share in its early stages. You can do all the research and speculate on various data, but it may all be for nought. Only in hindsight do we notice it.

- However, it is easy to identify when a crisis has hit, namely when an event has hit the share prices of companies to drop significantly.

Events?

- Political & geopolitical events can cause multiple stocks to drop, even though there might be nothing wrong with the company itself. The market is simply reacting in unison.

- Sector specific events can cause stocks from one sector to drop because news may impact that sector specifically harder than others.

- Company specific events may cause one company to drop whilst others (competitors) to rise.

Second core message: the first investment to consider is an ETF before an individual stock. It offers more diversity and risk spread and is a perfect tool to build investment security.

Perfect time?

- It is very unlikely that you will find the perfect moment to invest or sell a stock. Therefore, instead of trying to time the market, take the chance of investing when it has dropped, so you don’t miss the chance one it has recovered.

Asset classes

- The asset classes that every investor should look at includes: (i) stocks (ii) precious metals and (iii) real estate (optional)

- The first two should definitely be considered since they are more accessible with lower capital contribution requirements.

- The assets offer the following qualities for your portfolio: stocks (growth), precious metals (security) and real estate (stability).

Cycles:

- Each of these assets has its own up and down cycles. However, the cycles do not run in parallel with one another.

- Some are delayed and only happen after another asset class cycle has already moved significantly in its cycle whilst another move acyclical to the other classes.

- Therefore, if you invest in more than one asset class you can use the opportunity to build some wealth in one asset class (when it hits a high) and then reinvest in another asset class that has dropped.

- Alternatively, you can simply invest additionally available resources in the other downtrodden asset class, whilst not selling the others.

Chapter 5 – Where to get the money to make investments (pg. 109)

Companies are obligated to prepare a set of financial statements (balance sheet and income statement) on an annual basis for its investors. This gives its investors an overview over how the money of “their” company is being utilized.

Private investors would be well advised to also prepare a modified version of these statements so they can see:

- What assets do they have

- Differentiate between liquid (cash, shares, bonds, precious metals) and illiquid assets (real estate, art, jewelry, etc.)

- Which liabilities (debts) do they

- Differentiate between good (loans against assets which earn money) and bad debt (consumer loans)

- What are their monthly earnings

- Earnings from salary, rental income, dividend income, other income

- What are their monthly expenses

- Differentiate between fixed (costs incurred monthly with limited room for savings) and variable expenses (costs incurred monthly but not at the same amount necessarily)

Using this information, the investor can plan how to put some of their monthly income to productive use and invest it. Also, they can identify expenses that are not needed and can be cut off.

The most suggested approach is to take a % of your monthly income (once it hits your bank) and put it away immediately (i.e. paying yourself first) so that you can ensure a specific amount is invested per month and not consumed away.

Chapter 6 – Goals motivate for Wealth creation (pg. 125)

Set yourself some goals!

Why?

If you set yourself a goal it is easier to follow through with saving money than saving money for no specific goal.

A study by Harvard in the 1970s found that 3% of studies had set (wrote) themselves clear and specific goals whilst the other 97% either didn’t write goals or wrote goals that weren’t specific. When those studies were interviewed again multiple years later, it was found that those 3% of students had achieved their goals to a higher degree.

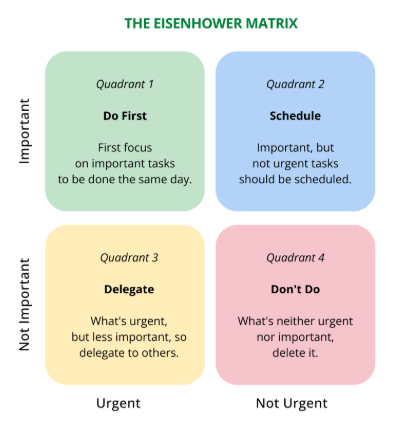

What tools can you use when you have many goals to achieve?

One approach – the Eisenhower matrix:

Every private investor is responsible for themselves and therefore they should use their limited resources (money) to invest the most effective and efficient way for the best results.

To make goals more effective, they need to be written and set up in a certain manner, which makes achieving them more real. Here the investor can use the SMART tool to write them down:

- S pecific

- M easurable

- A chievable

- R ealistic

- T ime

Chapter 7 – The magic of simple investing (pg. 136)

Chapter 8 – The three solid asset classes (pg. 144)

The top asset classes to invest in include (i) shares, (ii) precious metals (especially gold) and (iii) real estate. Since the first two don’t require a large investment, they are very suitable to most individuals. Furthermore, they are more liquid and would require little additional work from the investor since they don’t have a tenant or property damage to deal with.

Why gold and shares would be a good starter combination?

Both assets have cycles:

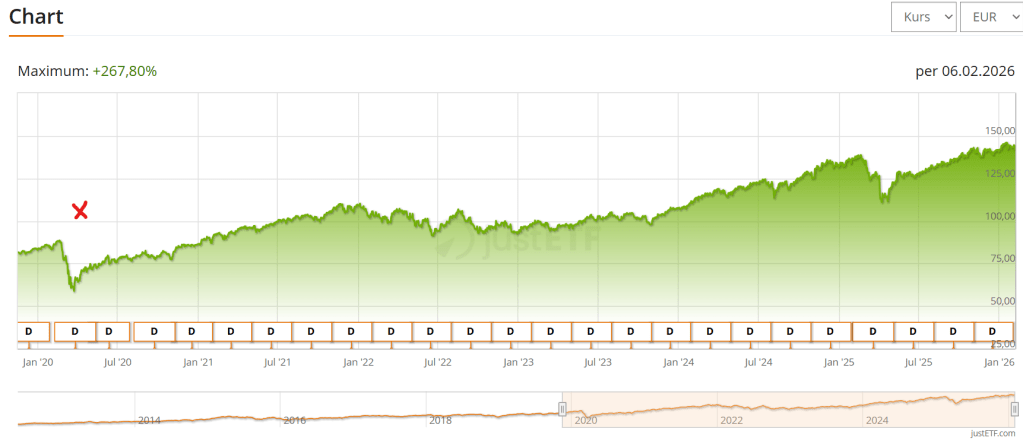

See a share cycle (ISIN IE00B3RBWM25 – Vanguard FTSE All-World UCITS ETF)

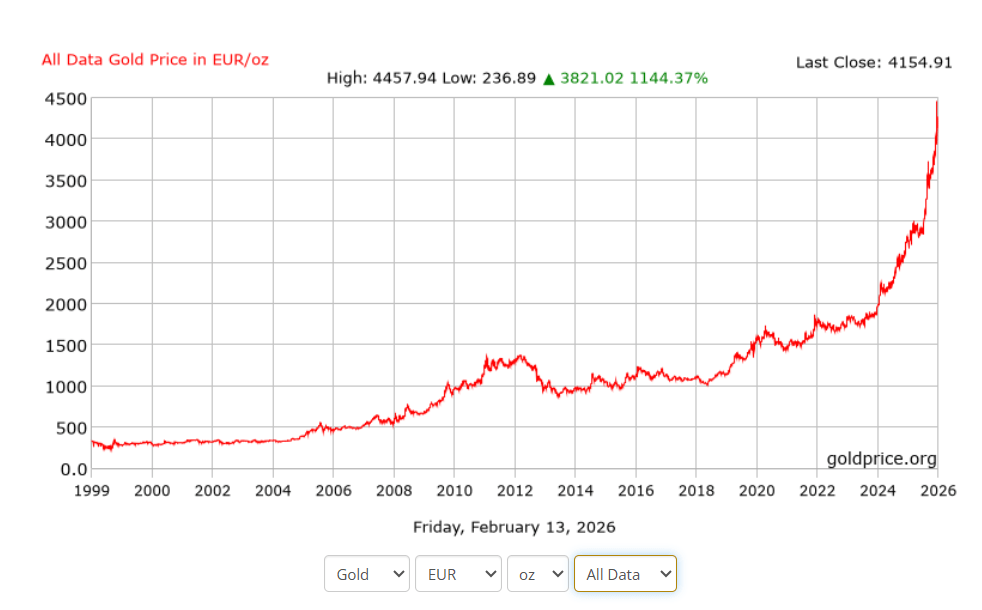

See gold cycle (https://goldprice.org/gold-price-history.html)

However, both have completely different cycles and don’t run in parallel. The objective of the private investor should be to invest in both classes. During phases where gold is running high and shares are priced lower, the investor can sell off some gold and invest in shares. Then, during phases where shares are priced very high, the investor can sell off some shares and invest in gold again.

However, as can be seen from the chart above, gold is relatively boring for long periods of time. Mostly it experiences a hype when there are big tensions in the world and investors wish to retreat to the crises currency.

The private investor should take away from these charts that the two asset classes, over time, both gain more value. Therefore, they are worthwhile investments. However, a combination of both is better than a focus in one. Furthermore, if they cost more, it means that the current medium of exchange (EUR, USD, CHF, GBP, etc.) is losing purchasing power. Thus, money is not the best way to save since it loses value in relation to other asset classes.

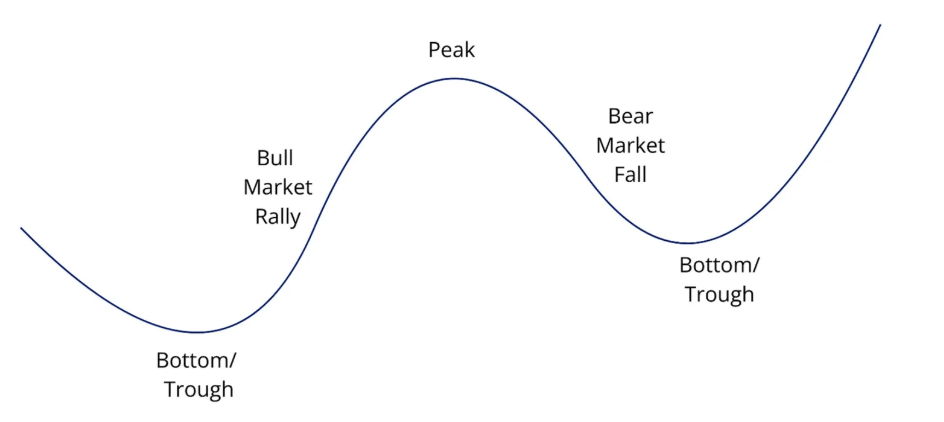

Chapter 9 – Typical cycles in each asset class (i.e. the four phases) (pg. 203)

Over the short term, the market price of assets can move up and down frequently. The cycle has four stages it can reach:

However, over the short term, the price is very unstable and is not optimal for private investors that wish to build long term wealth.

The optimal choice is to invest over a long term, over which it become more likely that asset prices will grow.

Chapter 10 – How to identify bubbles and use them (pg. 207)

Chapter 11 – What to learn from the past (pg. 210)

The past experiences (your own as well as more distant stock experience) should be used carefully when making investment decisions for today and the future. Simply because something worked in the past is no guarantee that it will work in the future.

Even though cash is more safe and stocks bear some risk, over the long term, stocks have outperformed most asset classes. The longer you remain invested in the stock market, the less the movements will impact your portfolio on average.

Chapter 12 – Be careful of overweight (pg. 212)

The private investor should be careful not to become over-invested in one asset class, since any sudden stock movements can leave a bigger dent in your portfolio than when your portfolio is spread widely.

This also applies to investing in specific sectors or countries.

Chapter 13 – Your investment plan in steps (pg. 214)

First, set up an emergency fund for those expenses that come unexpectedly. It would be sad to sell off some of your investments whilst they are down in value.

Second, money that is invested should be invested uninterruptedly for a long time horizon. Thus, if money saved will be needed in the next few months or years, then it should not be invested in the stock market. Only money not needed for at least ten years should be invested.

Third, differentiate between core investments and learning investments. Core investments should make up 80% of invested funds and learning investments are optional and should make up a maximum of 20% of your investments. The learning category allows you to experiment a little and hopefully learn something so that you don’t become too bored with the simple unexciting core investments.

- Core investments -> Shares (ETFs) ; Precious Metals (Gold)

- Learning investments -> Shares (single stocks) ; Precious Metals (Silver, other)

Fourth, start right away in setting up your investment plan and don’t delay it for much longer. Time literally costs you investment returns!

Closing (pg. 227)

Summary:

The book provided invaluable insights into a multitude of topics (asset classes, diversification, psychology, etc) which all are needed to understand that investing for the layman is a long term journey that can be quite profitable. Many books may emphasize the importance of diversification and starting right away (mostly ETFs), but this books also stresses the importance of opportunities in a crises. It is a worthwhile read, even if you have already read so many books on the topic. For this it will receive a rating of 4.75 / 5.

Enjoy!