Title: Mastering Market Cycles (Getting the odds on your side)

Author: Howard Marks

Hi all,

my final read for the year is on analyzing the economic and market cycles of the economy of your country. It is another strategy on investing, and most likely one that most intelligent investors make their most wealth by. The goal is to recognize when asset are sold cheaper than what they are worth and then buying them.

Value investing (followed by Warren Buffett) similarly has ties to this strategy.

But from the start, the author gives strong emphasis that this method is not very easy because it relies on making a bet on a pre-determined probability, and seeing what the real outcome is. Since the determination of this probability is difficult to pull through, they advise every investor to tread with caution.

Introduction

As humans we like finding the patterns in events, so that when we are confronted with the start of an event that we have encountered before we don’t have to consider what to do every time from scratch, but rather identify the pattern and then follow a method we followed before that worked.

- Companies and economies operate in cycles

- If we pay attention to cycles, we can get out ahead.

- If we 1) study past cycles, 2) understand their origins and import, 3) and keep alert for the next one, then we don’t have to reinvent the wheel in order to understand every investment environment anew

In order to get the most out of this, one needs to attain the following:

- Technical education and understanding in accounting, finance and economics

- A view on how markets work

- Reading is an essential building block

- Exchanging ideas with fellow investors

- No substitute for experience

I. Why study cycles?

The book argues that there is no means possible for anyone to accurately forecast the future. Therefore, the only other approach available for investment success is to have the following:

- trying to know more than others about that which is knowable: ie. the fundamentals of industries, companies and securities

- being disciplined as to the appropriate price to pay (possibly including a margin of safety) for a participation in those fundamentals

- These two elements constitute the fundamentals of value investing (ie. getting to know everything there is to know about the company, and then determining the price that you would pay to acquire a share in the company)

- understanding the investment environment we’re in, and deciding how to strategically our portfolios for it

- The word that is key to this is understanding “tendencies“

- studying past cycles to understand how they came about, and then what happened so they would turn around

- After gaining that understanding we identify where we are in the current cycle, then determine which next outcomes could happen, and the probabilities that each one will happen (tendencies = all possible outcomes * probabilities)

Therefore, the future should be viewed not as fixed, but as a range of possibilities and on a probability distribution.

—– this is the knowledge advantage that you should be looking for

II. The Nature of cycles

Another mindset change that the book introduces is that the life of a cycle shouldn’t be viewed merely as each being followed by the next one, but as each one causing the next.

Over the Long Term, economies have shown to grow on a small %, but this is not evident as we only consider the Short Term cycles in which we are currently living, which is a reflection of growth and declines, where the overall growth isn’t evident.

- The magnitude of the peaks and troughs is caused by the involvement of people as a result of psychology

The details of every cycle vary – the timing, duration, speed and power of the swings, and the reasons for them – but the underlying dynamics are usually similar.

- Most people think of cycles in terms of the phases as shown above and recognize them as a series of events

- But that’s not enough

- The events shouldn’t be viewed merely as each being followed by the next, but as each causing the next

III. The regularity of cycles

Our efforts are directed at trying to explain the world through the recognition of patterns. However, this effort of recognition of patterns is complicated, largely because the world we live in is beset by randomness.

There are a variety of factors that may influence the outcome of events, and due to this it is difficult to accurately predict the right outcomes.

IV. The economic cycle

The main measure of an economy’s output is GDP (Gross Domestic Product), which amounts to the total value of all goods and services that were produced in the domestic region. When more goods & services were produced than in the prior period then the country would be in an upswing phase. (However, bare in mind that we also need to remove the effect of inflation in order to get the real growth, not the nominal growth.

- growth or decline is attributable to the productivity (total output i.t.o. goods produced and total hours worked) of the population

The factors that influence growth in the long term don’t change significantly. However the factors that result in short term fluctuations (which result in peaks and troughs) can be attributed to investor’s psychology, emotion and decision-making processes.

- one thing that influences the short term decisions can be attributed to the “marginal propensity to consume”……if consumer’s have faith in the economy, they will spend more of every dollar on consumables. Likewise, they might invest more.

V. Government involvement with the economic cycle

Extreme economic cyclicality is considered undesirable by the governing body of a country. Therefore, the central bank is responsible to maintain stable growth of an economy, using the tools at its disposal, nl. raising/dropping interest rates, selling/buying securities and reducing/increasing the money supply (ie. monetary policy).

- before, their sole role was to accept gold and issue currency in exchange so that users may spend money in the US economy

- today, they have received the added responsibility to support the generation of employment, in addition to their current role of keeping inflation stable

Government’s tools and roles are to stimulate the economy by using fiscal policy (taxation and government spending on public programs).

VI. The cycle in profits

Another economic concept the book introduces is that goods and services being classified into elastic and inelastic category.

- Inelastic goods/services – when the economy is in a downswing or upswing, the demand for the goods/services is not influenced significantly. The goods/services can generally be classified as basic goods

- Elastic goods/services – when the economy is in a downswing or upswing, the demand for the goods/services is influenced significantly. The goods include luxurious goods/services.

However, the correlation between the profit/loss cycle of a company and the growth/decline of the economic cycle is not directly related. Meaning, when the economy is growing, the company might take a while longer to change into its profit stage due to other factors, which we can identify through the operating leverage and finance leverage.

This is best illustrated below:

Sales – Variable Production Costs = Gross Profit

Gross profit – Variable and Fixed Non-Production Costs = Profit (EBIT)

EBIT – Interest expense = Profit (EBT)

Operating Leverage = change in sales vs change in EBIT

Financial Leverage = change in EBIT vs change in EBT

- An entity may be selling more (and the economy is in its growth stage) however, the entity first needs to cover its production and non-production costs, and thereafter cover its finance costs (from loans) before it can write a profit

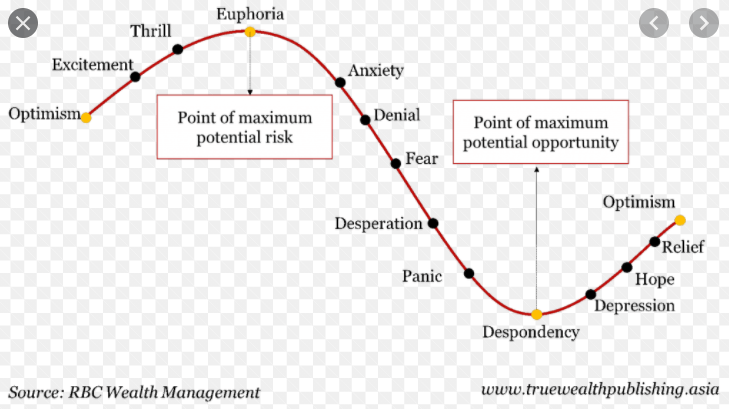

VII. The Pendulum of Investor Psychology

In business, financial and market cycles, most excesses on the upside and inevitable downside are the result of exaggerated swings of the pendulum of emotion/psychology

— when markets are on the rise, we see the actions and emotions on the left

–when markets are on the decline, we see the actions and emotions on the right

The too-strong upward and downward swings of the cycles (ie. their magnitude) largely results from psychological excesses in action. Thus, understanding and being alert to excessive swings is an entry-level requirement for avoiding harm from cyclical extremes

The superior investor a) performs a thorough analysis of investment fundamentals and the investment environment. He b) calculates the intrinsic value of each potential investment asset. And he c) buys when any discount of the price from the current intrinsic value

- In addition to the interrelatedness if the various emotional swings, it’s also important to note the causal nature of the phenomena. We all receive the same sets of data and information, however, our interpretation thereof (ie. positive outlook or negative outlook) and those of various other market players is what results in the strong market movements.

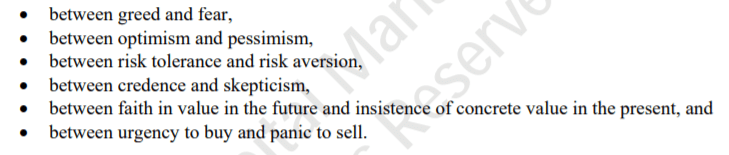

VIII. The cycle of attitudes towards risk

The rational investor is diligent, skeptical and appropriately risk-averse at all times, but also on the look-out for opportunities for potential returns that more than compensate for risk.

Risk = you have encountered a similar event before and know a few of the outcomes that may come about.

Uncertainty = you haven’t encountered a similar event before, but only know that you could lose your investment, or make a potential return.

For an investment you would lie somewhere in between the following range:

Certainty ————————-Risk—————————–Uncertainty

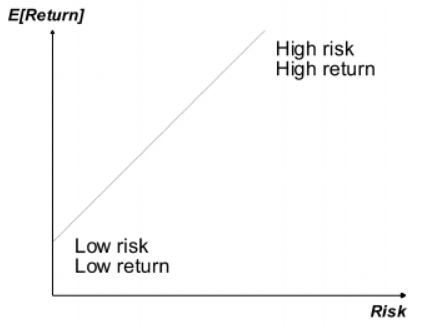

—The graph’s above depiction showcases that there is a direct relation between taking on more risk in order to generate a greater return. However, the graph is incomplete, and therefore not an accurate presentation of all the possible outcomes that may come from the investment. Instead, the graph should show some additional pathways/outcomes that the investment may end up in, so that the investor can distinguish between low risk, and higher risk investments that have multiple possible outcomes.

The concluding argument therefore lies with an investor always maintaining low-medium risk tolerance mindset, so that they won’t make too hasty decisions and not make decisions driven by emotions. Maintaining this mindset, he can evaluate for opportunities better.

Warren Buffett – When others fail to worry about risk and fail to apply caution, we must be more cautious. When other investors are panicked and depressed and can’t imagine conditions under which risk would be worth taking, we should turn aggressive.

IX. The credit cycle

The subject here is also referred to as the capital cycle. The cycle that shows when capital (ie. funds for investing) is made available for borrowing, vs when it is not easily accessible.

Observing this cycle is also a good indicator of where in the economic cycle we are, and where we are heading towards.

- availability of money supply

- interest rate for borrowing

Superior investing doesn’t come from buying high-quality assets, but from buying when the deal is good, the price is low, the potential return is substantial and the risk is limited.

X. The distressed Debt cycle

When the economy is entering a difficult and distressed time, few companies would borrow them money. Therefore, identifying when companies are going through this stage, their company’s value drop. If investors identify such companies, and see that they have value, they may decide to invest with such companies.

XI. The real estate cycle

Every cycle is driven to the peaks and troughs by the investors’ mentality in the current market. However, what makes this cycle different is the product that is sold, namely a tangible asset. The general myth is that the price of this asset is safe and will always grow.

However, when we are entering a trough in these cycles, people eventually learn that the merit behind these statements won’t protect the investment when the purchase price was made at too high a price.

XII. Putting it all together – the Market Cycle

Our job as investors is simple: to (1) deal with the prices of assets, (2) assessing where they stand today, and (3) making judgements regarding how they will change in the future.

- Prices are affected primarily by developments in two areas: a) fundamentals and b) psychology

- Fundamentals can be reduced to earnings, cash flow and the outlook of the two, and are affected by many things

- Psychology – how investors currently feel about the fundamentals and value them

- If company prices were solely determined by the fundamentals (ie. quantitative) the prices wouldn’t fluctuate as much, and would be appropriately valued

- However, psychology (qualitative) is also something that influences the price of company shares, and due to the different expectations of different investors (ie. psychology) the price is influenced by more than solely their current earnings.

Past events and expected future events combine with psychology to determine asset prices. Events (fundamentals) and psychology also influence the availability of credit (capital), and the availability of credit greatly affects asset prices, just as it feeds back to influence events and psychology.

Phrase – What the wise man does in the beginning, the fool does in the end.

XIII. How to cope with Market cycles?

The investor’s goal is to position capital so as to benefit from future developments.

- The objective is clear, but the question is how to accomplish this.

Step 1 – Understand where the future is at its present moment

- To do this, you need an understanding of the basic nature of the cycles

- Equipped with this understanding, you then turn to the task of figuring out where we stand in the cycle

- We can turn to general valuation metrics (P/E ratio, Yields) and other fundamentals

Step 2 – Understand how other investors are behaving

= Thus, the key to understanding where we stand in the cycle depends on two forms of assessment a) quantitative (valuations), and b) qualitative. This will give us the insight to assess where we stand. However, from here we will need to assess what are the likely outcomes that are expected to occur from here onwards.

Equipped with this knowledge we can identify where we might stand in the cycle. After this we will determine an amount which we value the company at, and then at what we will buy shares in the company.

XIV. Cycle Positioning

Good timing in investing can come from diligently assessing where we are in the cycle, and then doing the right thing as a result (ie. which entails adopting the right risk approach, and the appropriate assets).

- Cycle Positioning – the process of deciding on the risk posture of your portfolio

- Aggressiveness – the assumption of increased risk

- Defensiveness – the assumption of decreased risk

- Skill – the ability to make decisions correctly on balance

- Luck – when randomness has more effect on events than do rational processes

- Asset Selection – the process of deciding which markets, market niches and specific securities or assets to overweight and underweight

XV. Limits on coping

We have discussed the approach above, and it is therefore imperative for the investor to be reminded that this method is not easy and should be approached with care.

XVI. The cycle in success

The important lesson is that everything that produces unusual profitability will attract incremental capital, until it becomes overcrowded, at which point its prospective risk-adjusted return will move towards the mean (or worse).

Bottom line – nothing, no approach, method, or investment works forever

XVII. The future of cycles

Economies and markets have never moved in a straight line in the past, and neither will they do so in the future. And that means investors with the ability to understand cycles will find opportunities for profit.

People aren’t bound by rules, and will always make decisions with emotions guiding them. Therefore, the market prices aren’t solely based on economic factors but also on psychological factors.

Summary:

I have learnt a few new things from this book, and also enhanced my understanding in some topics that i had known before. The book has enhanced the importance for me that getting to know a company, and calculating an intrinsic value are better approaches for finding good opportunities on the stock market than merely following the crowd and leaving it all to luck.

The guidance provided in the book makes it quite clear that the future cannot be clearly determined by anyone, not even specialists of big companies, and therefore motivates any investor to take the reins and get to learn more on investing.

I hope this will entice you to put more consideration into any investments that you may be planning to undertake going forward, and therefore reduce the potential losses.

All the best, and happy New Year 2021!!!